- Tesla saw 1Q deliveries fall short of expectations, leading to demand concerns. The key question is whether this is a temporary blip or an ongoing structural issue

- Based on the data we know today, I view the issues as temporary in nature and see strong longer-term demand driven by high customer satisfaction and strong market share within their existing products

- Model S/X weakness is concerning, but explained by the decision to stop selling entry-level models. An upcoming refresh mitigates this risk, but Tesla must demonstrate superior value to other models

- Tesla Network buzz ahead of the Autonomy Investor Day is overly bullish in my view, but Tesla could still financially benefit from a capable semi-autonomous driving system

- The path to a higher stock is driven by showing profitable demand that can fund the next growth initiatives - the China Gigafactory and Model Y. I believe this is likely to occur over the course of 2019

Overview

The principle debate around Tesla is whether the manufacturer can sell enough of their vehicles at an acceptable margin. This debate has heightened recently after Tesla reported lower-than-expected deliveries in 1Q for both the Model 3 and the S/X, and after several seemingly abrupt price announcements over the last three months.

To be clear, I view Tesla as a materially riskier stock today than it was at the beginning of the year, and it is therefore trading at a deserved discount to those levels. The simple fact is that deliveries were lower in 1Q. We can name tens of reasons for why this might be the case, but we will not know with more certainty if this is temporary or the start of a longer trend until we get more data points on 2Q.

With that said, my own view is that Tesla is more likely than not to see a rebound in demand for the remainder of the year. I believe near-term demand has been impacted by a number of cyclical and temporary factors, but that longer-term, demand should ramp as awareness grows and customer satisfaction remains high.

I also believe that profitability will remain at acceptable levels to keep free cash flow (FCF) positive for the remainder of the year (beyond 1Q). Growing production, growing autopilot attachment rates, and elevated ASPs should all sustain acceptable operating margin for Tesla.

With sufficient demand and margins, Tesla should be able to maintain positive FCF levels while funding its next major growth initiatives: the Shanghai Gigafactory and the Model Y. With the growth story humming along, I believe it is more likely that the stock will move higher throughout 2019.

Unpacking the 1Q Deliveries Shortfall

The primary concern for Tesla is that near-term demand has slowed. Is this the start of a longer-term trend, or is it a temporary blip due to other issues? If it is a structural issue and demand for Tesla’s vehicles is not as high as Tesla and the bulls believes it is, it would stress their cash balance, force a dilutive capital raise, and call into question Tesla’s other growth initiatives. If it is a temporary blip, then Tesla should see a rebound in demand in the coming quarters and continue to develop its next major growth products.

The concerns heightened around Tesla’s 1Q production and delivery numbers reported in early April. Tesla reported 1Q deliveries of 63,000 vehicles, below consensus of 74,900. The shortfall was in both its luxury vehicles, as well as its higher volume Model 3 product. However, the degree was more drastic in S/X as deliveries of 12,100 fell short of consensus of about 20,000. Model 3 deliveries of 50,900 was also short of 55,100 consensus. Compared to 4Q, total deliveries were lower by 31%. (Note: for access to historical financials and forecasts, see my Tesla model, which reflects consensus estimates as of a couple weeks ago)

While results fell short, it was not necessarily unexpected. Earlier in the quarter, demand concerns heightened in January and February after US deliveries were estimated by several publications. Additionally, Musk made a number of seemingly hasty announcements, including the closure of (initially) all of its stores, then dialed back to many of its stores. The thinking was that he would not have made these announcements if demand was strong.

First, I think it's likely that these concerns are valid, and that demand was weak in January and February. Deliveries were much lower in the US, even for the slowest months of the year. According to Inside EVs, S/X volumes in January and February were weaker by 16% on a y/y basis, which takes into account seasonality. Additionally, it is difficult to reconcile Musk's quick actions to close stores and get the $35K model out. Yes, Musk is known to make quick, drastic decisions (see his funding secured tweets). However, if demand was strong, it's difficult to see why Tesla would announce a $35K Model 3 and announce the closure of its retail stores, shortly after having opened several retail stores just weeks ago.

To be fair, some of these actions were telegraphed by Musk and Tesla previously. For example, in late October, Musk had noted that they were “probably less than six months” away from a 35K version, and management’s 4Q guidance did note that deliveries would be lower in 1Q. However, it is clear that results came in below management's expectations for deliveries (as the production and deliveries report noted “lower than expected delivery volumes”), and I see it as more likely that there was some demand weakness, especially in January and February.

At the same time, it's important to disentangle how much of the weakness was due to temporary issues vs. structural demand issues for Tesla products. And I think temporary issues were likely a major factor behind the slowdown due to the following reasons:

Logistics issues slowed deliveries and disrupted the business dramatically. We know that Tesla faced a variety of logistical issues in getting the cars delivered to customers, like misprinted labels in China. With a backlog of cars produced and not yet delivered, Tesla likely faced a significant working capital drag, since the company would have spent cash to get the cars produced, but was not able to collect the cash on the sale until the car was delivered. As a result, it is plausible that Tesla would have had to slow production (and deliveries) until the logistics issues were sorted out. Wolfe Research noted, in meetings with IR, that Tesla was selling every car they could produce. This further supports the fact that the lower deliveries observed in 1Q was not completely a structural demand issue. Note that management themselves noted this in the delivery press release and several times ahead of the report (once during their $35K press conference, and during their 4Q conference call in late January).

Electric vehicle (EV) pull forward from December. Tesla noted on the 4Q earnings press release that the scheduled EV tax credit reduction would pull forward some demand from 1Q19 into 4Q18. There was also a tax credit expiration in the Netherlands which may have played a factor as well.

Industry slowdown in January and February. It was widely reported that industry vehicle sales were weak in January and February. The exact amount depends on what kinds of cars you include and exclude (i.e. retail sales vs. fleet sales, cars vs. light trucks), and the adjustments you make (i.e. number of selling days), but most reports highlighted a decline in the low to mid single digits. In a typical year, January and February are already the slowest months. Layer in the additional weakness, and we get very low volumes. Possible attributions noted by industry experts included cold weather (both January and February) and the government shutdown (January). This impacted the EV industry as well (see images below) and likely impacted Tesla volumes.

Normalized demand in 4Q sales was high. Tesla noted in 4Q that 75% of sales were new orders, suggesting that normalized demand is higher than what was seen in January and February. While some of this was likely helped by the pull forward mentioned above, it would be abnormal to see that degree of new orders, and then a sudden drop in the coming months without any material change to the product.

Long-Term Demand Paints a More Positive Picture

Cyclical or temporary demand issues are still demand issues, but they also suggest that Tesla's sales are likely to rebound in the coming future. Considering all these factors, I think demand was weaker in 1Q, but that it will pick up in the remainder of the year. My confidence stems from the following reasons.

Customer satisfaction is at industry-highs. Tesla’s customer satisfaction is the key long-term factor. Several consumer studies have shown that Tesla has the highest customer satisfaction among all auto manufacturers. In February, Consumer Reports gave Tesla an 89 out of 100 on owner satisfaction based on its extensive surveys - the top score in the industry. Additionally, Sanford Bernstein’s own survey in March examined 276 Tesla owners and found that 87% of respondents “loved” their Tesla.

Some of the reasons for this high satisfaction are characteristics that are inherently tied to EVs, like the fast acceleration, or the quiet ride. While these are competitive advantages today, they are not necessarily longer-term moats, as auto manufacturers will eventually make their own EVs with similar benefits (as I discuss later).

However, the reasons for high customer satisfaction also extends beyond electric vehicle characteristics. Primarily, Tesla emphasizes the customer experience, and it’s apparent in numerous features. For example, Tesla doors automatically unlock when approaching them, and the company recently added new features to the car like Sentry Mode and Dog Mode. While these features by themselves do not sound significant, they do add up to a holistic experience that leave customers with a positive impression. Auto customers have been trained to expect a static product that still looks and feels much like the same product 10-20 years ago. Tesla’s vehicles are a refreshing new product in a stagnant industry.

Source: The Last Driver License Holder

A happy customer can be forgiving of the most glaring issues, at least to a point. It was also Consumer Reports that removed its “recommended” rating after publishing low reliability data for the company. This aligns with numerous other reports that have circulated among social media and mainstream media articles. Even with lower-than-average reliability though, consumers remain satisfied. So long as satisfaction remains high, the company will get more wiggle room from customers than other auto manufacturers. That’s not to say that reliability concerns are not an issue for Tesla. The company must get ahead of the problem before more long-term damage is done to the brand, and it’s a crucial risk that all bulls must watch closely. However, I can’t help but wonder if bears are overestimating the seriousness of Tesla’s reliability issues, at least in the near-term.

High satisfaction has translated into strong market share. The high overall satisfaction ultimately translates into strong market share within each segment Tesla participates in. According to IHS data, Tesla owns ~15% market share of the $60K+ global luxury sedan market with the Model S and roughly 8% market share of the global luxury SUV market with the Model X. And Model 3 demand of 200K-400K units globally would imply a roughly 10-20% market share of the global $40-60K sedan market (with current 2019 consensus of 270K units placing model 3 market share at 12%).

Given still-high customer satisfaction, and the market share trends seen in other segments, it is difficult to see why demand trends would suddenly drop off after a 4Q in which 75% of orders were from new customers and not from the backlog.

The total addressable market for the Model 3 is enormous. The luxury sedan segment is a large market and suggests room for higher volumes for Tesla. The global market for $40K-60K sedans was just over 2 million vehicles last year, according to IHS data. Within that market, Audi, BMW, and Mercedes all sell vehicles at much larger volumes on an annual basis, and with lower customer satisfaction than Tesla. The BMW 3-Series sold about 400,000 units on average over the last 4 years (note that 2018 volumes were about 10% lower, likely due in part to the Model 3), and has a $40K average selling price (ASP). The Mercedes C-Class sold almost 500,000 units, also with a ~$40K ASP. And the Audi A4 sold almost 400,000 units at a $37K ASP. At higher price points of around $50K, each manufacturer has similar volumes of 200-400K units (i.e. the BMW 5-Series, the Mercedes E-Class, and the Audi A6).

Furthermore, the total addressable market is likely even more broad than those numbers would suggest. Tesla has noted that they are seeing trade-ins from numerous other segments, including SUVs and non-premium vehicles. As an illustrative point, there were over 4 million sedans sold between the $30K - $60K price range globally, according to IHS data.

It’s important to note that there are some structural issues for EVs that could limit the numbers a bit more than the numbers might suggest. Not all customers have access to home-charging, for example. However, it seems more than achievable for Tesla to sell at similar volumes as any one of those manufacturers’ models with a product that makes more owners happy.

Tesla is just beginning to pull several other demand levers. As management has discussed, Tesla still has a few “levers” that could boost demand:

Leasing. Tesla recently announced leasing terms for the Model 3, so this isn’t necessarily a lever anymore, but more of a tailwind that should help drive more demand in the coming quarters. Leasing has historically made up anywhere from 30% to as high as 50% of demand (for luxury vehicles), according to Edmunds data. And Tesla's leasing for the S/X has historically made up 20% of sales. As stated on their 4Q conference call, Musk noted that leasing would have a negative impact on GAAP financials. However, given that analysts often make adjustments to GAAP financials anyway, this is more of a superficial issue that should not affect the stock.

Marketing. This is perhaps the biggest lever. Tesla currently doesn’t have a paid advertising budget. While customer satisfaction is high for existing Tesla customers, there is still an awareness gap with the rest of the market. Many people still don’t know how electric vehicles work. Tesla currently relies on word of mouth from its avid fan base - an effective tool, but also a slow one. Tesla could meaningfully accelerate demand simply by investing in paid advertising. While this would obviously come at a cost, it is a better to have demand outstrip supply than to have demand fall short of production capabilities, if that were to occur.

S/X Demand Looked Weaker in 1Q. Is Cannibalization the Issue?

As noted previously, S/X demand was significantly weaker than expectations. Given that S/X vehicles carry gross margins in the high 20s, the concern is that the shortfall will pressure auto gross margins and overall profitability, not just in 1Q, but for all quarters going forward.

There are a few counterarguments to the shortfall. First, and perhaps most importantly, Tesla discontinued its entry level S/X vehicles in early 1Q. These vehicles represented a large portion of total units (perhaps 50% of volumes), and likely impacted demand significantly. Tesla may have discontinued the vehicles in anticipation of an S/X refresh, which has been rumored for some time, and appears to be picking up steam. If this is true, it would suggest that 1) S/X sales were weak primarily due to Tesla's deliberate decision to stop entry-level S/X production ahead of the refresh, and 2) the upcoming S/X refresh could reinvigorate sales.

Additionally, as mentioned previously, the EV tax credit expiration and industry weakness in January and February could have hampered S/X volumes. And with high trim model 3's shipping internationally, these vehicles could have cannibalized S/X sales globally. As Tesla begins to ship lower trim models internationally over time, perhaps the cannibalization effect has a smaller impact on overall volumes in future quarters.

Bears would argue that these arguments do not explain the weakness fully. If the tax credit pulled forward demand for the S/X, why were S/X sales in 4Q not artificially boosted even further than what we saw? Deliveries in 4Q were strong (and Tesla noted that they achieved all-time high market share in the US in 2H18), but they did not appear to be abnormally high on an absolute level (see image). Either it benefitted from a pull forward (and saw structurally lower demand during that time), or it did not pull forward demand, and 1Q weakness is not due to the pull forward. Either way, we get weakness in one quarter or the other. And given that S/X is often sold at prices of around $100K, would a $7,500 tax credit reduction really move demand that much among that demographic?

Finally, if the S/X refresh was planned, why was this not baked into more conservative guidance for 1Q? Management simply said that they expected S/X deliveries in 1Q19 to be “slightly below” 1Q18’s deliveries of 21.8K units. But if management had planned to cancel its high volume entry level versions, you would think that their guidance would have been more conservative.

Overall, this is a difficult one to judge; the bear arguments are fairly convincing, but if Tesla actually did discontinue the entry level S/X in order for the upcoming refresh, then perhaps this is not a reliable sign of weak demand, but rather a conscious choice by Tesla management. In this instance, I think management may have just underestimated how severe the decline would be without the entry level models. And in fact, rumors around an S/X refresh have been picking up more recently. Ultimately I think this is a mitigated risk once the S/X refresh comes out, but it could present downside to Tesla if they are not able to meaningfully differentiate the S/X from the 3/Y.

Will other auto manufacturers catch up?

Will other auto manufacturers be able to make compelling electric vehicles that can compete with Tesla? My own view is that 1) traditional auto OEMs are not taking EVs as seriously as the bears argue, and 2) even if they are, a growing EV market would benefit Tesla, not harm them.

Auto manufacturers are not taking EVs seriously. Electric vehicle competition from the traditional auto manufacturers is not as strong as it might seem. While announcements have been numerous, the field has yet to produce an electric vehicle that is competitive on paper with Tesla’s vehicles, and in volume.

No vehicle that is actually in production is competitive yet in terms of acceleration, range, and cost. Note that there have been several vehicles with announced specs that looked attractive. However, the actual specs within the production vehicle has consistently fallen short. For example, the Audi e-tron’s actual EPA rating of 204 miles in range fell well short of its announced range of over 310 miles in 2015. As counterintuitive as it might sound, the traditional automakers’ engineering quality is not up to par with Tesla’s. Automakers are not designing EVs from the ground up, leading to suboptimal decisions.

Volume is also a key consideration. While there have been some vehicles that look potentially attractive to consumers, such as the Hyundai Kona, they have not been produced in meaningful volumes. A key constraint is battery production. With most automakers relying on LG chem for batteries, they’re not able get the volumes that are needed to seriously compete with Tesla.

Looking more deeply into why the automakers are falling short shows that the level of commitment to EVs is not there. Specs fall short because the automakers are not designing cars from scratch. Volumes fall short because automakers have not decided to get more involved in the battery production themselves like Tesla has (note that while Tesla does not produce the batteries, they do have longer-term agreements in place with Panasonic). Some production plans have been put in place, but are not expected to come online until the early-to-mid 2020s. While the automakers have made splashy announcements, few have actually made the hard financial decisions to compete effectively with Tesla.

One of the few companies that arguably has made a larger commitment is Volkswagen. CEO Herbert Diess has been vocal in his belief that EVs will become a larger percentage of overall industry volumes, and in praising Tesla’s actions. Mr. Diess’s comments on Tesla show why incumbent auto manufacturers struggle to make the commitment that Tesla has in EVs:

“I think Tesla is doing a good job. They don’t have to care about the legacy. They don’t have to care about the next generation of gasoline in motors and so they can really focus on the future. It’s an advantage.”

In other words, the legacy ICE business for traditional auto manufacturers prevent them from investing more heavily into EVs. Each dollar invested in EVs lowers the industry ROI. For each manufacturer, EVs are not as profitable as ICE vehicles currently (especially as they are not at the same scale), and they cannibalize a higher-margin ICE vehicle that is at scale.

Additionally, many industry experts believe that peak vehicle SAAR (seasonally adjusted annual rate) volumes are behind them, and that a downturn is ahead. In this environment, manufacturers are even more hesitant to make margin-dilutive investments.

As a result, many investors in the other auto manufacturers actually question whether they should be making larger investments in EVs and taking the space more seriously. As Sanford Bernstein wrote in a note to clients, VW’s “massive EV plans are bold...worryingly so” and that “almost no other OEM shares this view or vision.”

Auto manufacturers are increasingly looking at mergers and partnerships that could increase scale and potentially reduce the margin dilution. Examples include VW and Ford’s cooperation in light commercial vehicles, BMW and Daimler in ridesharing, and Honda’s investment in GM’s Cruise Automation. These developments require monitoring, but note that larger-scale moves would be risky and take time to integrate and play out.

Credible competition will eventually come, but it could actually benefit Tesla

Regardless of Tesla’s success, it is likely that incumbent auto manufacturers will eventually produce competitive EV vehicles, whether in the next 5 years, or in the next 10 years. Goldman Sachs, one of the most vocal Tesla bears on the street, forecasts electrified (battery plus hybrid) vehicles to account for 35% of global auto sales by 2030. Sanford Bernstein projects 9-17% electric penetration of global passenger vehicles by 2025, and JP Morgan projects 7.7% penetration by 2025.

Counterintuitively, this scenario is potentially more beneficial to Tesla than harmful, depending on Tesla’s ability to hold onto its market share. As the traditional manufacturers begin to focus more on EVs, they will need to invest in infrastructure and marketing to educate customers on the benefits of an electric vehicle. And as awareness of EVs grow, it could bring in more interested customers to Tesla. As an illustrative example, if a potential customer heard about Audi’s new EV, they would likely take a look at the current EV leader, as well as other EV offerings, as part of their research before making a final decision. Tesla would effectively be able to piggyback off of other manufacturers’ marketing efforts. In other words, a growing pie can offset share loss.

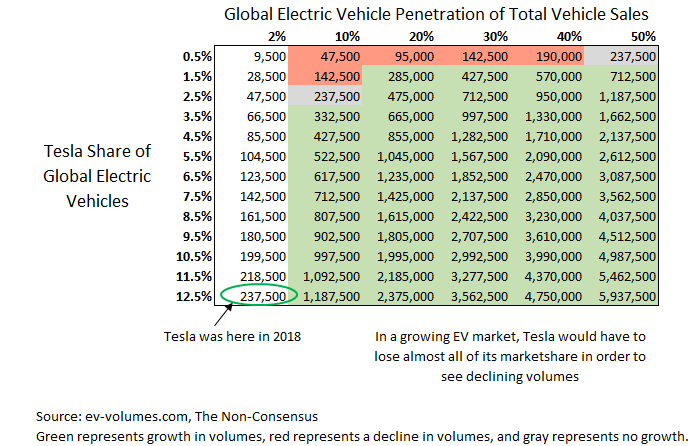

The following graph illustrates this point. Assuming that EVs grow to 20% of the global light vehicle market at some point, Tesla would need its EV market share to drop from today’s 12.5% to less than 1.5% in order for volumes to decline. To be fair, Tesla does not need to see declining volumes for the stock to decline; decelerating growth would accomplish a similar stock drop. However, with that said, the chart still shows that it would take significant share loss in a growing EV market for growth to slow. These scenarios seem less likely given that almost all of the success in the EV industry is being driven by Tesla.

Autopilot Does Not Need to Achieve Full Self Driving to Become a Key Competitive Advantage

There has been a somewhat separate line of debate between bulls and bears around Tesla’s autopilot business, which Elon Musk has been pushing as a key component of Tesla’s longer-term growth plans. The debate revolves around the value of the business and whether it will achieve fully autonomous capabilities. Elon Musk has recently stated on Lex Fridman’s AI podcast that Tesla was ahead of the competition and will be achieving feature-complete self-driving capabilities soon.

On one hand, numerous bears, and many experts in the AI community, have argued that Tesla is well-behind in self-driving capabilities. Google’s Waymo is widely perceived as the leader in the space with the fewest disengagements per mile, some progress towards commercialization (with Waymo One), an army of machine learning experts, and a first-mover advantage. Meanwhile, Elon has made numerous promises (including a cross-country drive that was supposed to happen by the end of 2017) but has yet to live up to his statements. In an era of loud, visionary startup leaders that make bold, borderline-fraudulent statements (see Theranos and Fyre Festival), many are fairly skeptical.

In my view, this is an interesting line of debate that is rife for additional investigation. Many of the street analysts are largely taking the conventional wisdom that Waymo is ahead based on superficial analyses, but are not diving deeper. There have been numerous people more deeply involved with disengagement data that have argued that the data is too easily manipulated to be of much use as a measuring stick for progress. Additionally, several passengers in Waymo One have noted that they have seen drivers taking control of the vehicle on several occasions.

I am admittedly not well-equipped to opine on who will achieve full autonomy first, or how long it will take. With that said, I view the autopilot feature from an investing lens in two ways.

First, Tesla does not need to achieve full autonomy to reap financial benefits. Tesla’s current self-driving features remove a significant mental burden for long commutes. While drivers still must monitor the vehicle and be ready to take over at all times, the mental drag is lower than if one were driving the vehicle fully. This is a strong feature that could change the way we see driving and what we expect out of our cars. And unlike full autonomy, this is available today and a much less daunting task to improve upon. As this feature becomes more widespread, it could become “table stakes” - in other words, it could be expected in a vehicle for it to even be viable as a potential purchase.

To be fair, other vehicles today offer certain degrees of autonomy. For example, many systems can manage braking, steering, and acceleration. However, few vehicles offer a more holistic experience like Tesla. Additionally, without over-the-air (OTA) capabilities, manufacturers cannot improve on its autonomy features over time. This latter point is key given that an autonomous/semi-autonomous vehicles are expected to get better with time. For now, I would argue that Tesla has a lead in commercialization (for level 2+) and a competitive advantage over other vehicles.

As a result, Tesla does not need to achieve full autonomy in order to recognize the value of its autopilot program. With its current autopilot capabilities today, and projecting out modest, ongoing improvements, Tesla has a key differentiating feature in its vehicles that 1) benefits sales and differentiates Tesla vehicles further from the competition, and 2) benefits gross margin significantly.

Second, while I am not yet in the camp that Tesla will achieve full autonomy soon, I do view the possibility as a call option on the stock. Tesla’s approach is meaningfully different from the other auto OEMs and software companies, in part because they hold a key asset: data. Tesla decided to forego LIDAR, and equipped all of its vehicles with OTA capabilities. These decisions gave Tesla a fleet of vehicles (affordable to the consumer) that are capable of collecting data that could then be used to further train its neural net. It is not yet clear to me if having more data will ensure that Tesla will achieve full autonomy first. However, it seems like a real possibility given that more real-life data is often a key factor in improving performance for several different machine-learning approaches. Because Waymo is not able to collect enough data on real-life edge case scenarios, they are forced to hand code the proper response. Meanwhile, Tesla is potentially able to use its extensive data (which presumably holds many more instances of certain edge case scenarios) to train its neural net for the optimal response.

It’s important to appreciate just how difficult it is to solve full autonomy. Much of the game-changing features, like having a car that can earn money for you in the Tesla Network, comes in having no driver at the wheel of a car. But for this to be achievable, the vehicle needs to be able to handle all sorts of long-tail events in a safe way that also balances the passenger’s need to get to their destination in a timely manner. Think about it this way: over your last two weeks of driving, how many times did you come across a long-tail scenario that required you to break the rules of driving, and to use a more generalized knowledge of the world? And how many times might one come across these scenarios while driving 250,000 - 500,000 miles (the typical distance a human driver will drive before getting into an accident)? To achieve full self-driving, and for it to not be disruptive on the roads, an autonomous vehicle will need to know how to handle all of these situations quickly, and safely.

Due to this difficulty, I’m not yet ready to start baking in autonomous driving products (like the Tesla Network) into the valuation of Tesla as a whole - hence the call option view. At the same time, I also believe that semi-autonomous driving can still prove to be a meaningful differentiator for Tesla vehicles, and a gross margin benefit. And the stock could meaningfully appreciate if Tesla makes further progress in getting towards full autonomy.

As a result, autopilot developments should be monitored closely, and investors can start with the Autonomy Investor Day that is expected to occur on 4/22 (which is perhaps the day this article is published). Going forward, if Musk’s statements are true, Tesla’s autopilot improvements should become more rapid now that Hardware 3.0 is rolling out to more vehicles.

The Gross Margin Puts and Takes

Tesla must also show that there is sufficient demand at an acceptable level of gross margin. This has become an even larger point after Tesla’s announcement of the $35,000 Model 3, which Tesla has hinted at in the past as not yet being profitable. It would not be beneficial to Tesla if they are only able to show that sufficient demand exists at a price point where gross margins are negative.

There are several puts and takes here, but there are enough data points to suggest that Tesla can stay profitable:

Numerous sellside analysts have come away from Fremont factory tours confident that the company can continue to grow production to 7,000 per week with minimal incremental capital expenditures. Several have noted that numerous parts of the factory were built with scale in mind (Wedbush, Canaccord, Macquarie as examples). Increasing production volumes should drive gross margin expansion.

Management noted that maintaining gross margin above 20% should be achievable with ASPs in the mid to high $40K range. This appears doable given that Tesla’s peers (BMW and Mercedes) all have similar ASPs.

One question that could be key in the near-term is how different gross margins for high-end Model 3s and entry-level S/X's are. Based on what we know, they may not be too dissimilar, based on the following: 1) High end model 3's have gross margins north of 20%, 2) Model S/X, inclusive of all trims, have gross margin in the mid to high 20s (based on data prior to when the model 3 went on sale, as well as management commentary), 3) Tesla was only shipping high trim Model 3 vehicles internationally in 1Q19 (the 20%+ gross margin models), and 4) Tesla discontinued the entry-level S/X at the beginning of the quarter (which are likely to be below the overall S/X gross margin of mid-to-high 20s). If gross margins for the high-end model 3 are similar to the entry-level S/X, then we could potentially see a modest surprise in 1Q gross profit, as it is perhaps not as horrible as some might fear. Consensus currently calls for 19.6% auto gross margins, excluding ZEV credits.

The US had about 100K units of high-trim Model 3 demand (in 3Q and 4Q). With a larger appetite for luxury sedans in the EU, and an enormous Chinese market that has yet to be fully tapped into, it seems feasible that global demand for high trims could be at a similar level. With an estimated 30K delivered already in 1Q (50K total Model 3s delivered minus the 20K Model 3s reported to be delivered in the US), this would imply that we could see another quarter or two of high-trim demand internationally. The mix benefit could offset the mix headwind from the $35K Model 3 deliveries in the next several quarters (which has now been moved off-menu).

As mentioned previously, Autopilot and Full Self Driving provides a significant gross margin boost, and could alter the margin trajectory as the service improves over time. Tesla’s decision to make autopilot a standard feature in all vehicles should provide a meaningful benefit. As an illustrative example, a Standard Range Plus with a 5% gross margin would generate a 16% gross margin with the Full Self-Driving package.

On the negative side, gross margins are likely to dilute over time as the Model 3 mix shifts towards lower ASPs over time. Additionally, we could see further cannibalization if Tesla does not manage its good-better-best offerings carefully with the Model 3/Y and the S/X. And of course, if demand falls short of production, we could see further margin headwinds and potentially other price announcements to incentivize customers to purchase.

Tesla Needs to Demonstrate Profitable and Sustainable Demand to Fund Its Next Leg of Growth

Tesla’s growth plan is to continue to expand into other categories (like the $40-60K SUV segment with the Model Y) and continue to capture similar market share levels as their current products. For the stock to work, Tesla must continue to fund the next expansion and demonstrate continued demand in each segment.

Naturally, Tesla’s largest step-ups in revenue have also come from the launch of new models into new segments. Looking at Tesla’s history, the largest revenue gains have come once the new models began volume production. And the largest stock movements have similarly come sometime between the announcement of the next model and the volume production ramp.

Thus, the key to the Tesla growth story lies in its ability to fund its next legs of growth. Two of the primary growth drivers in the near-term are the Shanghai Gigafactory and the Model Y. Tesla expects the Shanghai Gigafactory to drive an additional 3K/week in Model 3 volume (or roughly 150K units per year). Additionally, Elon Musk has discussed his expectation for the Model Y to have even higher volumes than the Model 3, with numbers potentially as high as 800K/year once fully ramped. Note that Tesla has several other upcoming products, including the Roadster and the Semi. However, these two are not expected to drive as much revenue growth (given more limited volumes), and Tesla has yet to discuss more concrete plans for these products.

The bear thesis is that Tesla will not be able to sufficiently meet demand at a sustainable margin, and that the company will not be able to fund its growth plans without dilutive capital raises.

Importantly, I don’t view a future capital raise as a negative event, depending on the circumstances. If raised from a position of strength (i.e. Tesla proves that underlying demand for its products remains strong and raises capital to introduce more products), then it could potentially be received positively by investors as a de-risking event and further acceleration of Tesla’s growth plans, even with the dilution. If raised from a position of weakness (i.e. Tesla runs low on cash amidst demand issues), then a capital raise would certainly be a more negative sign. In my mind, the more important factor is how demand is shaping up, not whether the capital raise occurs.

With this in mind, the path to a higher Tesla stock over the next several quarters involves the following:

Prove that sustainable demand exists for the Model 3

Prove that the vehicles can be produced at a sustainable gross margin (high-teens to 20%) level and that operating margin can stay positive with enough investments to maintain a growing fleet

Maintain positive FCF while funding its growth initiatives

With all risks considered, I view this as the likely path for the company and would advocate building a position in the stock.