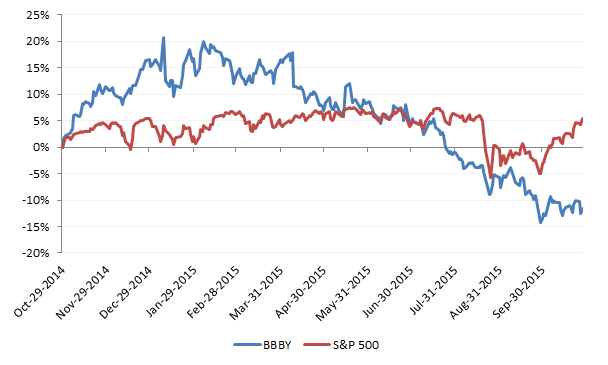

Over the last year, Bed Bath & Beyond has declined 12% vs the S&P 500's 5% gain. I detailed the bear case for Bed Bath and Beyond back in mid February, and the bear case has largely played out since that time. Going forward, a key issue will rest on whether BBBY will be able to re-accelerate its top line growth, and how quickly.

Key Issue 1: Top Line Woes

Bed Bath & Beyond's comps have continued to come in just at or below expectations. In their latest 2Q results, the company reported comps of just 0.7%, which came in below company guidance of 2% - 3% and consensus expectations of 2.1%. Additionally, the company reduced full-year comp guidance from 2% - 3% to 1% - 2%. Importantly, traffic declined for the first time since 1Q14. Online sales grew over 25%, but it was clearly not enough to offset store weakness (online sales are included in the comp number). However, gross margin did come in slightly above expectations in the quarter.

Bed Bath & Beyond appears to be in a tight spot where they either get hurt either on gross margin or on comps. If they mail out coupons to drive sales, their gross margins are hurt. If they don't mail out more coupons, their traffic and same store sales are hurt (this appears to have happened in 2Q). At the heart of the issue is increased competition and Bed Bath & Beyond's commoditized merchandise. The company believes consumers are going online to find cheaper products elsewhere, and is doing a number of things to combat the sales slowdown, including:

- Growing its assortment in adjacent categories like jewelry, luggage, mattresses, furniture, and watches

- Making investments in analytics to drive increased personalization of products

- Increasing the assortment of differentiated products, with help from their other concepts (buybuyBABY, Christmas Tree Shop, World Market)

While these initiatives are encouraging to hear, given multiple years of <3% comp growth, investors need to see these investments pay off in the form of higher sales / reduced gross margin pressure before rewarding the stock. As a result, a key debate will be whether management's efforts to turn sales around and reinvigorate its customer base are working.

Key Issue 2: The Cost of Re-Accelerating Sales

While management attempts to turn sales around, investors are keeping a close eye on the impact on margins. As detailed in my prior post, Bed Bath & Beyond's margins have been pressured from increased promotions as well as investments in building out its online capabilities. Going forward, investors are already expecting margin pressure as the company continues to invest in the initiatives mentioned above. However, expectations are for those margins to gradually bottom out over time, settling at around 11.5%.

A key question will be how much the company will invest in itself. This question will likely be tied to the success of their existing initiatives; if they are not successful, the company may have to spend more and margins may fall below current expectations. Longer-term, there is also a concern around the idea that e-commerce may simply requires a heavier level of recurring investment to keep up with other companies (Wayfair, Amazon) that do not operate stores and invest fully in their website.

Key Issue 3: Share Repurchases and FCF Level the Silver Lining

Offsetting many of these concerns is BBBY's capital allocation. Senior management has repurchased a significant amount of shares over the last several years, which has allowed EPS to maintain growth despite a decline in net income (see chart below). Going forward, management has authorized an additional $2.5 billion share repurchase program after the completion of its current program. If management continues to repurchase shares at this level, it could offset some of the operational weakness in the business.

The general counter to this bull argument is that share repurchases is a low-quality earnings driver. If operating income continues to decline, Bed Bath & Beyond's free cash flow will likely decline as well, as it has over the last several years (FCF declined 20% last year and is expected to decline 12% this year). With FCF declines, management may decide to repurchase fewer shares going forward because 1) they can't afford to repurchase as many, and 2) the capital may be better spent reinvested into the business to turn around operations. Again, a key component will be how the company's initiatives play out going forward, and whether they are successful in re-accelerating sales growth and settling margin declines.